It is a very common questions I get from buyers, ” What are the closing costs?”. I thought it would be a good idea to include a very generic list of some items that may be included in your closing costs, an estimate as to what they will be and also what that money is going towards. I do want to stress the cost is different for every transaction and will depend on the home you are purchasing among other factors.

I ran across this awesome list on Zillow.com. The full list can be found here. **I didn’t include everything on the list that Zillow has on their website.**

- Appraisal (up to $450) – This is paid to the appraisal company to confirm the fair market value of the home.

- Credit Report (up to $30) – A Tri-merge credit report is pulled to get your credit history and score. You cannot supply your consumer pulled report and the scores pulled form the internet from any place other than myfico.com are not real scores nor are they accurate.

- Closing Fee or Escrow Fee (generally calculated a $2.00 per thousand of purchase price plus $250) – This is paid to the title company, escrow company or attorney for conducting the closing. The title company or escrow oversees the closing as an independent party in your home purchase. Some states require a real estate attorney be present at every closing

- Title Company Title Search or Exam Fee (varies greatly) – This fee is paid to the title company for doing a thorough search of the property’s records. The title company researches the deed to your new home, ensuring that no one else has a claim to the property.

- Survey Fee (up to $400) – This fee goes to a survey company to verify all property lines and things like shared fences on the property. This is not required in all states.

- Flood Determination or Life of Loan Coverage (up to $20) – This is paid to a third party to determine if the property is located in a flood zone. If the property is found to be located within a flood zone, you will need to buy flood insurance. The insurance, of course, is paid separately.

- Lender’s Policy Title Insurance (Calculated from the purchase price off a rate table. Varies by company) – This is insurance to assure the lender that you own the home and the lender’s mortgage is a valid lien. Similar to the title search, but sometimes a separate line item.

- Owner’s Policy Title Insurance (Calculated from the purchase price off a rate table. Varies by company) – This is an insurance policy protecting you in the event someone challenges your ownership of the home.

- Homeowners’ Insurance ($300 and up) – This covers possible damages to your home. Your first year’s insurance is often paid at closing.

- Escrow Deposit for Property Taxes & Mortgage Insurance (varies widely) – Often you are asked to put down two months of property tax and mortgage insurance payments at closing.

- Transfer Taxes (varies widely by state & municipality) – This is the tax paid when the title passes from seller to buyer.

- Recording Fees (varies widely depending on municipality) – A fee charged by your local recording office, usually city or county, for the recording of public land records.

- Processing Fee (up to $1,000) – This goes to your lender. It reimburses the cost to process the information on your loan application.

- Underwriting Fee (up to $795) – This also goes to your lender, covering the cost of researching whether or not to approve you for the loan.

- Loan Discount Points (often zero to two percent of loan amount) – “Points” are prepaid interest. One point is one percent of your loan amount. This is a lump sum payment that lowers your monthly payment for the life of your loan.

- Pre-Paid Interest (varies depending on loan amount, interest rate and time of month you close on your loan) – This is money you pay at closing in order to get the interest paid up through the first of the month.

- Property Tax (usually 6 months of county property tax)

- Wood Destroying Pest Inspection and Allocation of Costs – If required by the lender or buyer, the inspection generally runs up to $125.00. Repairs can get expensive if evidence of termites, dry rot or other wood damage is found. example: Fumigation of a typical 1500 square foot house could run around $2,000.

- Home Owners Association Transfer Fees – The Seller will pay for this transfer which will show that the dues are paid current, what the dues are, a copy of the association financial statements, minutes and notices. The buyer should review these documents to determine if the Association has enough reserves in place to avert future special assessments, check to see if there are special assessments, legal action, or any other items that might be of concern. Also included will be Association by-laws, rules and regulations and CC & Rs. The fee for the transfer varies per association ,but generally around $200-$300.

Again, I want to remind you that the costs will be different in every transaction and this list is just to give you a better idea of what might be included at closing. Please call me if you have any questions about closing costs.

Thanks for reading.

(photo taken from

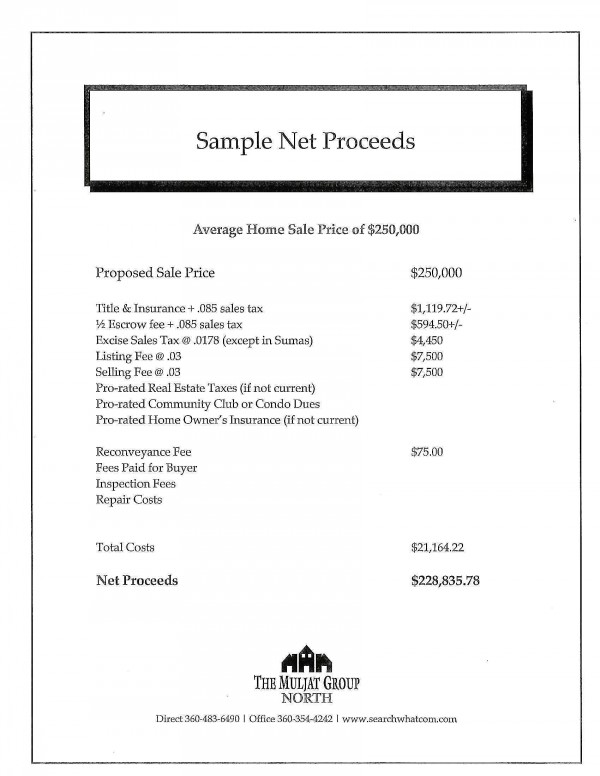

(photo taken from  If you are curious about what the cost would be to sell your home please give me a call. I have a formula all set up on my computer that will help me calculate an estimate of what your net proceeds would be. Just need a few minor details. (No strings attached ☺)

If you are curious about what the cost would be to sell your home please give me a call. I have a formula all set up on my computer that will help me calculate an estimate of what your net proceeds would be. Just need a few minor details. (No strings attached ☺)